Rabobank report upbeat on fruit, tree nuts

The RaboResearch report cites a drop in input prices, a better water outlook in California and improved logistics. Tree nut prices, pushed downward due to elevated inventories, are seeing a much-needed lift, according to the report.

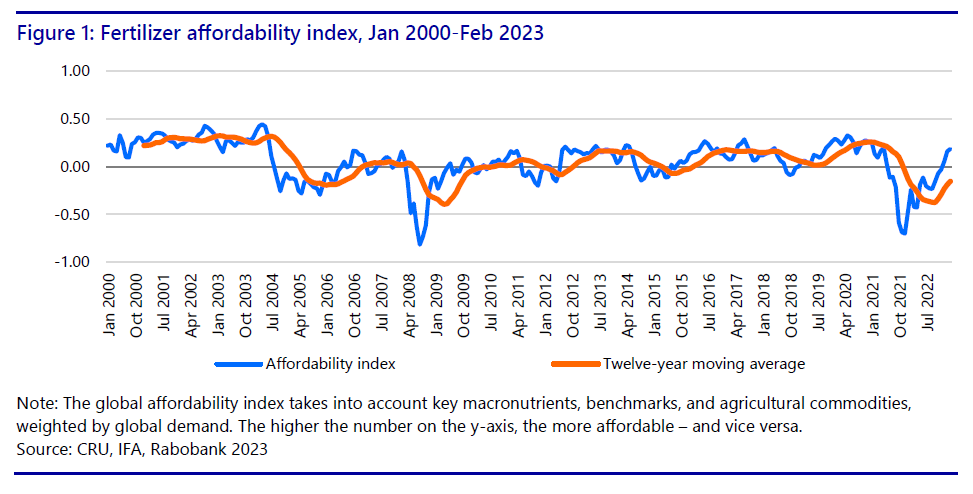

Global fertilizer prices

U.S. fruit and tree nut producers know that when it comes to global fertilizer prices, a rising tide lifts all boats. The cost structure of the fertilizer complex is driven by high-demand commodities such as corn, soybeans, and wheat. Given the relatively small percentage of global demand for macronutrients that fruit and tree nuts represent, they are subject to these major agri-commodities’ influence on prices.

Click to enlarge

In the wake of the Russia-Ukraine war and Belarusian sanctions, global fertilizer prices skyrocketed in 2022, exacerbating global affordability to levels comparable to 2008. As was the case then, the resulting demand destruction (along with today’s improved trade dynamics) precipitated a fall in fertilizer prices as markets moved from panic to trading closer to fundamental supply and demand.

Input costs easing

Since the third quarter of 2022, fertilizer price momentum has been largely downward, the consequence of which can often be a slow proliferation through the value chain of the products. Though this slow movement through the value chain is most evident in pure-play commodity products — such as urea, DAP/MAP and MOP, for example — the negative price trajectory could improve the cost structure for many of the specialty inputs used in fruits and tree nut production.Where the bottom lies for these macronutrients depends on many factors that are yet to be determined by the markets. Still, there are indications that prices for both potash and phosphate could continue to fall in the medium-to-short term.

However, with demand picking up in the Northern Hemisphere as we head into the planting season, we may see some bumps in the road. Replacement costs for many agrochemicals appear to be drifting lower as seaborne logistics costs ease and Chinese production continues to improve. Supply concerns for agrochemicals in the North American market, particularly for generic products, appear to have subsided. Abatement in the most severe cost inflation environments, with cost constraints easing for the most marginal producers, could ultimately mean improved yields and productivity.

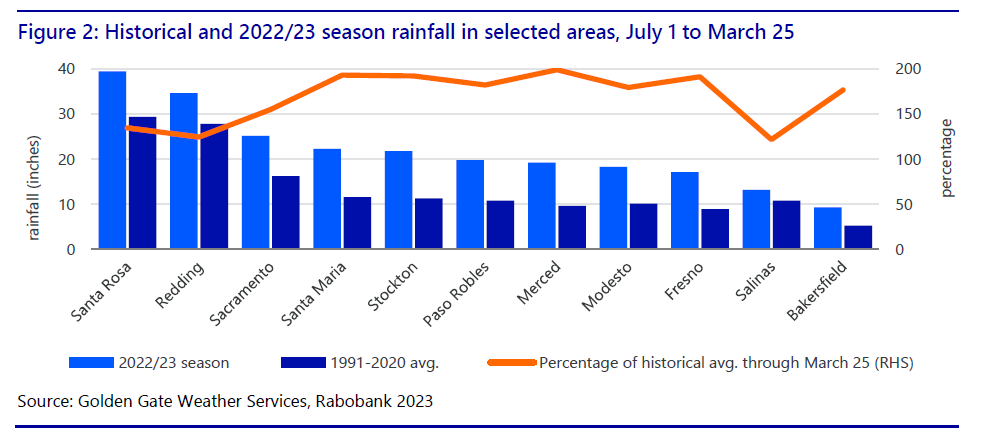

Improved water conditions in California

The improved water outlook has come at the short-term cost of increased use of herbicide and fungicide in some crops to manage a wetter environment. In the longer term, however, current wet conditions will benefit farmers, particularly those who are able to maximize water banking for future dry years.

Click to enlarge

Logistics entering the shipping market

Challenges related to shipping and other logistical factors will be much eased in 2023 compared to recent years. We are seeing a downcycle characterized by overcapacity in shipping equipment and vessels. Prices have adjusted significantly down from their peak in 2021, although they are still likely to remain above pre-pandemic levels. Schedule reliability has greatly improved and is approaching pre-pandemic levels. Shippers will regain bargaining power as the supply-demand balance shifts toward oversupply over the next two years.Global indexed ocean shipping spot rates have largely returned to 2019 levels, driven by weak transpacific demand from China. However, blanked eastbound sailing limits the availability of containers for exports out of the US, leading to continued high costs for export containers. We expect ocean container prices to gradually decline but remain above pre- pandemic levels. We also expect contract prices to be less volatile, lagging spot rate changes by up to a year.

Domestic trucking spot rates have also fallen dramatically. This is mainly driven by a lack of demand for long-haul truckload, a different transportation category than most fruit and tree nut exporters use. Short-haul and less-than-truckload demand remain strong. This, combined with high fuel surcharges and ongoing labor challenges, will lead to less reduction in actual surface transportation costs and continued pricing pressure compared to pre-pandemic levels.

While high fuel surcharges may be transient, labor issues are structural for both the trucking industry and West Coast ports. This could significantly impact the reliability of fruit and tree nut shipments in the near term.

Packaging costs down

Although paper and plastic packaging prices have surged beyond inflation in the past few years, costs will likely stabilize or even decline over the next 12 to 18 months. Both the containerboard and relevant plastic resin markets face an oversupply issue with additional capacity from both domestic and foreign markets entering the U.S.In the short term, we expect a period of predictable packaging costs and stable packaging supply for fruit and tree nut exports.

In the long term, sustainability concerns around packaging, especially plastics, will continue to create cost and operational challenges for exporters. Recyclable and compostable options are available, but at higher prices and with lower barrier performance. Commercially viable sustainable packaging alternatives may still be several years away.

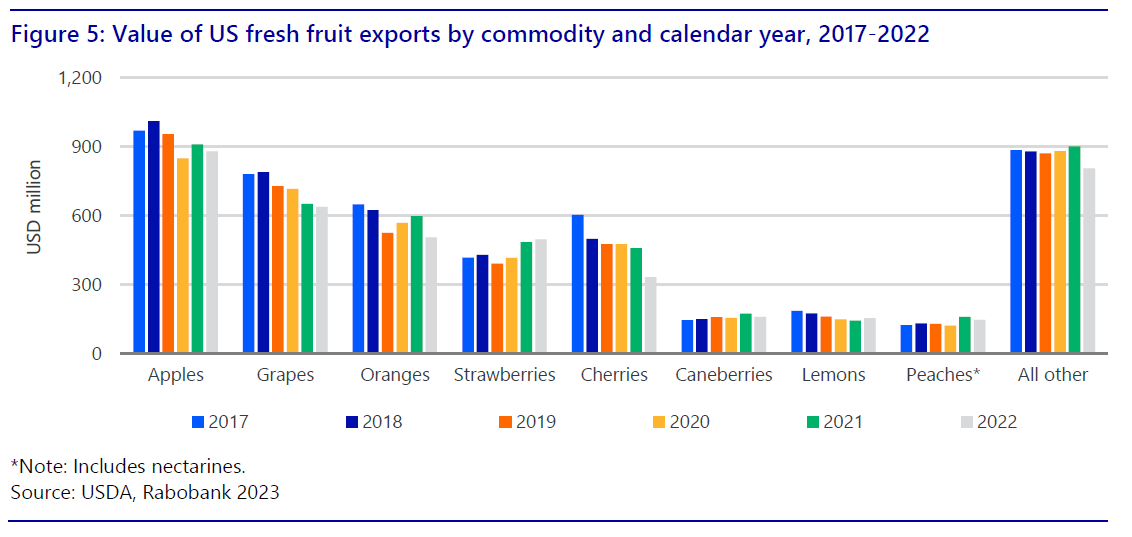

U.S. fresh fruit exports up to 2022

Exports are an important component of the U.S. fresh fruit industry. Over the past decade, the share of U.S. production that was exported (exports divided by production) has been as follows: 37% of fresh grapes and fresh raspberries, 32% of fresh oranges, 26% of fresh apples, 16% of fresh lemons and 15% of fresh strawberries. For most commodities, this share has been declining in recent years as domestic demand continues to increase.

Click to enlarge

U.S. fresh fruit exports have been declining — both in terms of value and volume — for the past few years. Particularly in 2022, relevant headwinds that impacted fresh fruit exports included lower fruit production in the Pacific Northwest due to a cold spring, logistics disruptions and supply chain bottlenecks, and an appreciating U.S. dollar, among other factors.

Canada is a relevant destination for U.S. fresh fruit exports, including apples, grapes, oranges, strawberries, cherries, and caneberries, while Mexico is a key market for U.S. apples and grapes. More distant markets that have a significant share of U.S. exports include Vietnam and Taiwan for apples; Taiwan, Australia, Vietnam, Japan and South Korea for grapes; South Korea, Japan and China/Hong Kong for oranges; South Korea, Taiwan, China and Japan for cherries; and Japan for caneberries. For a recent update on the strawberry market, see Rabobank’s recent report Strawberry Plantings on the Rise. U.S. apple exports to India have declined considerably since retaliatory tariffs took effect in 2018.

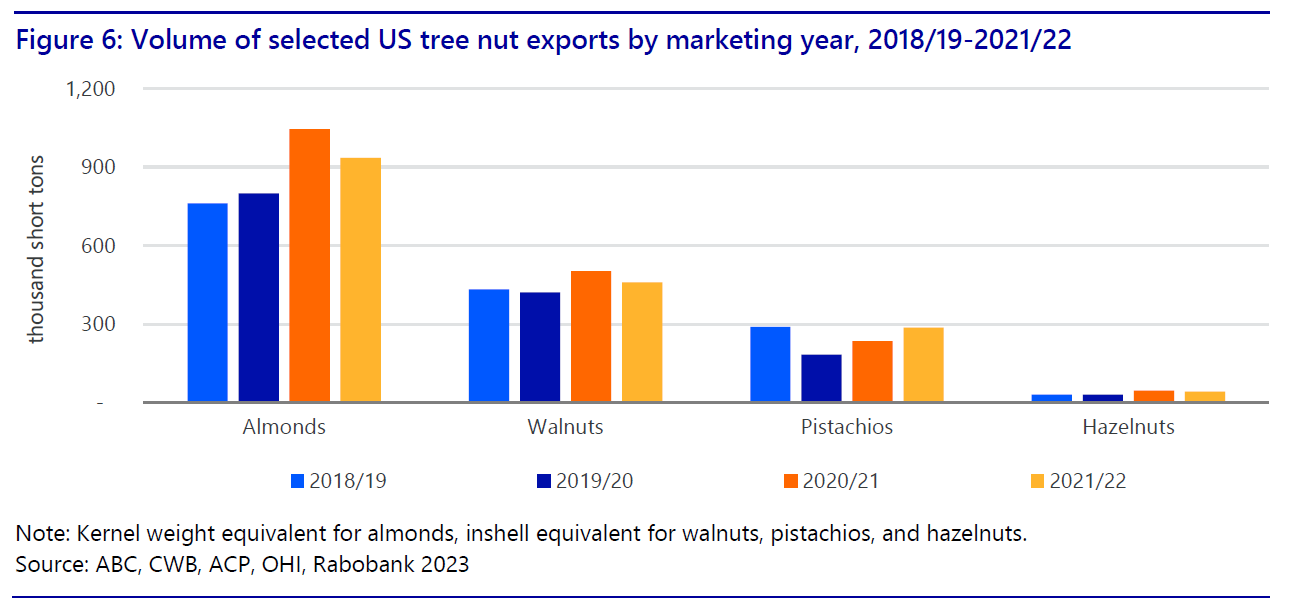

Tree nut exports lag behind production

Tree nut exports account for about 70% of U.S. marketable tree nut production. Destinations are diverse, with the largest share of shipments going to countries in Asia and Europe. U.S. almond production almost tripled from the early 2000s to 2020, surpassing the 3-billion-pound milestone ahead of industry expectations due to favorable growing conditions that year. The following two seasons saw some challenges, and production declined as yields were impacted by weather events and an irrigation deficit in some areas.

Click to enlarge

U.S. walnut and pistachio production also recently set production records. The unprecedented carry-in into the 2022-23 marketing season was an undesirable consequence of logistics constraints and subdued global demand.

U.S. tree nut exports set a record in 2019, surpassing $9 billion, according to the USDA. With prices under pressure due to increased inventories, the value of tree nut exports in 2022 was 5% lower than in 2019, despite a 12% volume increase. Shelled almonds and inshell walnuts were the categories with the largest decline in export value from 2019 to 2022.

According to industry data, exports of almonds, walnuts and hazelnuts were down 11%, 9% and 9% YOY, respectively, during the 2021-22 marketing year. Pistachio production set a record in 2021-22, but exports remained below the record set in 2018-19.

Tree nut exports, prices rising

Aided by improving logistics and other factors, U.S. tree nut exports have been showing better numbers in recent months. Almond exports for the 2022-23 marketing season are up about 12% YOY through March, with exports in December, January, February and March increasing 24%, 47%, 29% and 24% YOY, respectively. Walnut exports in January showed a 25% YOY increase, reaching a multi-year high volume for January. While the U.S. pistachio crop in 2022 was significantly lighter than in the previous two seasons, pistachio exports are up 7% YOY for the 2022-23 marketing season through February.Improving exports and the prospect of more manageable tree nut inventories at the end of the 2022-23 marketing season have been reflected in a much-needed price lift in the past couple of months. Another relevant factor that will influence prices in the coming months is the size of the 2023 crop. Almond yields will likely be lighter as cold and wet weather prevailed during the blooming/pollination season. Weather conditions are expected to be better for pistachio and walnut bloom periods, but it is too early to pin down yield expectations.